Ch 1: Present value

The discount rate links the present value to a future estimate

To practice finance is to assign prices to things. To assign prices, we need to be able to retrieve the present value by discounting future value(s). The future value can be a single value ($10 to be received in 24 months) or a set/scenario of estimated values (binomial tree, scenarios). The present and future values (PV, FV) are two of the five variables in the time value of money (TVM) construct. Incredibly, financial exams like the CFA and FRM still require calculators, and the most popular is the Texas Instruments BA II Plus (TI BA II+) calculator. The five variables in its TVM worksheet neatly occupy the third row:

In sequence, these keys map to the following Excel functions: NPER(), RATE(), PV(), PMT() and FV().

You probably already know how to discount a cash flow, but you may not be aware of a few technical points that will be helpful if our goal is mastery. Good finance is careful about terminology: precise thinking requires precise definitions. Or maybe I should say that good definitions lead to better thinking?

The present value is a theoretical price

The present value (PV) is what we can call a theoretical price. Let's say our asset happens to be a single share of ownership in a publicly traded company. Maybe we used a discounted cash flow (DCF) model to decide this asset's price should currently be $43.00. Simultaneously, perhaps we observe that the price trades on an exchange at $39.00. Our model says the share should be worth $43.00, but its market price is $39.00, so we can say "This asset is trading cheap". The theoretical price is its present value because we discounted future value(s) that are estimated or maybe even just guessed. Alternatively, if the traded price bids up to $47.00, we can say, "This thing is trading rich" because the observed price exceeds our theoretical price.

The theoretical (aka, model) price is not the observed (aka, market) price

Things trading rich or cheap is not abnormal, it is the typical condition. We do not expect the theoretical price to equal the observed (aka, traded or market) price. This distinction between model and market prices matters so that we do not get into the bad habit of expecting observed prices to match theoretical prices. Everything will trade a little or a lot rich or cheap. (For some deep reality, see yesterday’s great post by Aaron Pek). Models are not meant to be accurate. The theoretical price is merely the output of whatever toy model we happen to be using and its handful of factors; our toy model captures neither all of the relevant factors nor all of the dynamics that contribute to an actual price. Most models could be defined by the majority of known, omitted factors (before even considering unknown factors) rather than the few factors they explicitly do include! Our models should always be humble in this way. There can be many subjective model prices bouncing around as a function of users and their toys. But there is only one currently observed price1. Further, an interesting philosophical question is whether a single, unknowable intrinsic value exists at all2. That's philosophy before arithmetic.

The present value goes lower as the discount rate goes higher and/or the future goes further away

A mentor once said to me, "All of finance is basically bond math." Bonds are a great place to start because the theoretical price of a bond is its discounted present value. Say Acme is an industrial company that wants to borrow cash, so Acme issues a bond with a face value of $1,000. There are literally four synonyms for a bond's face value, alas. Specifically, this $1,000 face value can also be called a par value, the principal, or the redemption value. The investor is a lender who gives Acme cash but expects to be repaid in the future. In the time value of money (TVM) construct, this bond's face value is a future value (FV) because the investor expects to be repaid $1,000 in the future.

To keep it simple, we'll assume this bond pays no coupon interest in the meantime; i.e., prior to redemption. It is a zero-coupon bond. Maybe it is a 5-year bond which means that it will mature in five years and, at that future time, the lender expects to be repaid the redemption value (aka, face value) of $1,000. An exam question about a bond will either need to mention its maturity (e.g., five years) or—less commonly but more realistically—the question will need to provide the bond's maturity date; for example, if it matures on 2028-06-27 and today is 2023-06-27, then we know the bond has five years to maturity. Next year on 2024-06-27 the bond will have a remaining maturity--aka, maturity--of four years will its original maturity will always be five years.

But the $1,000 face value is a future value, to be repaid in five years (in our illustration). How much cash does the lender give the company today? In formal terms, we're asking, What is the bond's theoretical price? This is the same as asking, What is the bond's present value (PV)? To estimate the PV we need the discount rate. Let's say our discount rate is 8.0% per annum with annual compounding. We've got everything we need! The theoretical price of this 5-year zero-coupon bond is given by discounting the future (face) value to its present value:

$1,000 / (1 + 8.0%)^5 = $1,000 * (1 + 8.0%)^(-5) = $680.58

In Excel, we retrieve this value with the formula: =1000/1.08^5. Although it's unnecessary, we can also use a function: -PV(8%, 5, 0,1000) = 680.58. By our estimate, omitting fees and frictions, the lender will give Acme $680.58 today and expect to be repaid $1,000 (the face value) in five years. If we increase the discount rate to 9.0%, the theoretical price (PV) declines:

$1,000 / (1 + 9.0%)^5 = $1,000 * (1 + 9.0%)^(-5) = $649.93

And we just illustrated duration risk: the risk that the bond price will go down because the interest rate goes up. The lender, who is long the bond, is maybe a bit sad if this rate jump happens after she lends the money: she is still earning 8.0% but the market rate (an opportunity cost) is now higher. The borrower (Acme, who is short the bond) is maybe a bit happy: they are suddenly paying a below-market interest rate. If the interest instead drops from 8.0% to 7.0%, then the bond price increases from $680.58 to:

$1,000 / (1 + 7.0%)^5 = $1,000 / (1 + 7.0%)^(-5) = $712.99

Now the lender is happy and Acme is sad. In fact, if this bond were like a mortgage (with its prepayment option) and had an embedded call option, then Acme might call the loan and refinance the borrowing (with a new bond) at the lower rate.

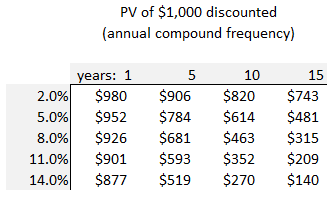

Therefore, the maturity (five years) and the discount rate link the present value (PV) to the future value (FV). Below is a common pattern. Assuming the same $1,000 future value, we discount at various rates and maturities. When we go out to 15 years, the present value drops dramatically and becomes very sensitive to the rate. You can imagine the role of the discount rate in climate science, even before wondering about the precision of future estimates: if the estimated damage is faraway in the future, a higher discount rate reduces the present value of the cost (and might reduce the urgency).

Before we finish, I'll share three technical points.

Interest rate is a vague term

Let's get professional with three points. First, the discount rate is an interest rate but "interest rate" or "interest rate factor" (the risk analog) turns out to be a bucket that contains many different types and flavors of rates. This bucket includes spot rates, forward rates, par yields, among others. Our discount rate is a spot rate (aka, zero rate).

Second, I specified the discount rate (aka, spot rate) in a specific way. I wrote: 8.0% per annum with annual compounding. Exam questions should be thusly specific. The per annum (aka, annualized) rate distinguishes it from a different periodicity such as 8.0% per month. However, here is an important convention: interest rate inputs and outputs should (almost) always be annualized. This avoids confusion. Theforefore, I could give the same assumption by writing "8.0% with annual compounding" because the reader can rightly assume the 8.0% is per annum. The reader (or candidate) should not be left to wonder, Is this per month or per quarter? We can assume it is per annum (per year). We serve readers an annualized rate, and we let them slice it into months or quarters to their own taste. When finished, the exam candidate should annualize the output.

For example, if this were a coupon rate instead of a discount rate, we should not write "4.0% every six months." Instead we write "8.0% per annum with semi-annual compounding" or, if we are comfortable, "semi-annual 8.0%" or even "s.a. 8.0%". Due to convention, we know this does not mean 8.0% twice a year; rather, it is an annualized (aka, per annum) 8.0%, which is 4.0% every six months. This 8.0% is also called the stated or nominal rate, but it is not an effective rate. The effective rate must be higher than 8.0% for any compound frequency that exceeds once per year. In summary, unless we have a good reason otherwise, in which case it should be clearly articulated, stated or nominal rates should be annualized as both inputs and outputs.

Third, the discount rate assumption of "8.0% per annum" is incomplete until we specify the compound frequency. Why? Here is the theoretical bond price if the discount rate, instead, is assumed to be 8.0% per annum with semi-annual compounding:

$1,000 / (1 + 8.0%/2)^(2*5) = $1,000 * (1 + 8.0%/2)^-(2*5) = $675.56

Although the nominal rate is 8.0% in both cases, the bond discounted with a semi-annual compound frequency is theoretically cheaper. Put more precisely, these are two slightly different discount rates even though the nominal rates are identical. The $680.58 and $657.56 bonds both share the same 8.0% nominal rate but their effective rates differ. The bond discounted at 8.0% per annum with semi-annual compounding has a lower present value (PV) than the bond discounted at 8.0% per annum with annual compounding. To recap this third point: a nominal rate is annualized (per annum) but the nominal rate is an incomplete specification until we also provide the compound frequency. Hence, the fully specified pattern (which can be abbreviated; e.g., certain instruments imply their frequency) for an interest rate is given by:

X% per annum with [annual|semi-annual|quarterly|daily] compound frequency

Summary

We've learned that the theoretical price of a thing in finance is likely to be its present value, although we are not surprised to observe a price that is trading rich or, alternatively, “trades cheap” relative to this model price. We saw that the present value becomes quite sensitive to the discount rate as maturity (distance to the future value) increases. We mentioned that we’re using a discount rate to retrieve the present value, but interest rate is a vague term (a bucket of various rates). Finally, we discounted the same 8.0% in two different ways: with annual compound frequency, then with semi-annual compound frequency.

In practice it’s not quite this straightforward. On various exchanges, buyers and sellers enter orders (e.g., market order, limit order) that inform bid-ask spreads. If the bid/ask is $12.33 / $12.37 then the spread is $0.04. But there still exists a midmarket price of $12.35.

On this question, I suppose I’m a phenomenalist rather than a realist: I do not think there is such a thing as a instantaneous value that is “true”; aka, current intrinsic value.