Stocks I own: Blackrock (BLK)

BLK is a titanic succulent worthy of holding (I'm at 2.0% allocation). Stock Rover's research report is attached, if you'd like to see an example of one of their tools.

I’ve been actively managing1 my public equities portfolio for years. I’m not sure it’s wise. There are two huge problems with active management: it’s time consuming2; and I’m mediocre at doing it. My best argument in favor stock selection is only indirectly financial: it’s a fabulous way to learn about commerce and markets. Unless you enjoy the learning that investing affords, I’m skeptical that anybody should actively manage their portfolio in a part-time role. Unless you are both really special and very hard-working, like Jonah Lupton for example, I wouldn’t plan on making a lot of money picking stocks. If I didn’t like learning about companies and markets, sincerely, I would probably just track his portfolio(s) as a sub-allocation3.

Some stocks are high-growth roses and some are low-growth succulents. Roses require constant attention because their valuation is fragile such that potential disappointment always looms. On the other hand, you can ignore succulents for months. Blackrock is one of my succulents. I haven’t updated my notes on BLK in over a year.

I bought BLK on 12/26/2018 for $361.41. At today’s price of $833.35 (+ 130%) that’s a 5.6-year holding period return of +157%. This translates into a price CAGR of +16.2% and a TSR CAGR of +18.1%. My current allocation to BLK is 2.0%. As you can see, dividends have contributed almost 2.0% of my TSR. BLK’s forward dividend yield is 2.48%. It is an appealing dividend grower and good candidate for a retirement portfolio.4

Instead of a deep dive into BLK, I will simply share5 Stock Rover’s Research Report on BlackRock. Stock Rover is my favorite stock research tool, but I do need an entire article to explain why (stay tuned for that …).

Like many investors in BLK, my original thesis concerned their leadership in the ETF market which has since expanded into so-called active ETFs. I added BLK at about the time I sold my banks: I wanted financial services exposure but my banks were too hard to analyze. Although it ranks 44th on Fortune’s Financials list (that I just got in my email), BLK is the largest asset manager in the world with > $10 trillion in AUM.

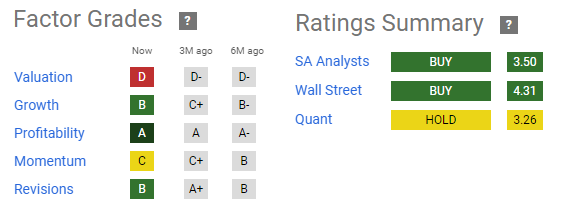

I do not usually focus on Seeking Alpha’s factor grades and ratings, but I find them interesting in BLK’s case:

None of the analysts (6 SA + 16 Wall Street) have Sell ratings despite the stock’s rich valuation (the D rating). The forward P/E is 19.74 which is a whopping +72% above the sector median, but it also matches BLK’s historical P/E. This is often the profile of a premium-priced market leader. I’ve read all the analysts and I sort of think it boils down to whether you think BLK is constrained by the Law of Large Numbers6 , or if you discern their breadth, depth and optionality as advantageous. I’m in the latter camp.

With Claude’s help, I reviewed the last five earnings transcripts. Here’s a few items that stick out for me, in no particular order:

Over the last five earnings calls, analysts have been focused on these metrics: AUM and organic base fee growth rate, net inflows by product category, operating margin, Technology services revenue growth and ACV, fee rate trends and share repurchase amounts. For these metrics, the trend is positive. This titanic succulent is still growing its AUM (now up to $10.6 trillion which is somehow +11.3 YoY!); growing its organic base fee (up from 2% to 3% with a long-term growth target of 5%); growing (or at least maintaining) its margins (eg., 2024 Q2 operating margin of 44.1% is +160 bps YoY); and growing its Aladdin technology platform (+10% YoY).

Interest rate sensitivity (this is always relevant to me but especially in the current moment): Black Rock basically has little or no directional exposure to interest rates. Lower rates benefit their fixed income ETFs and equity AUM; higher rates benefit their cash management products. Instead, rate regimes tend to increase the volatility of BLK’s businesses.

Private markets are one of their next big bets: Their planned acquisitions of Preqin and Global Infrastructure Partners (GIP) reflect aggressive expansion into private markets. On the last earnings call, the CFO said “the bigger longer-term opportunity is leveraging our engines in Aladdin and indexing with our capital markets expertise to build the machine for the indexing of private markets. What the creation of public benchmarks did to drive stock markets, especially visible through iShares, we believe the combination of BlackRock and Preqin can do for private markets.”

Artificial intelligence is not a dominant theme on calls. Rather, Larry Fink promoted AI’s relevance to BLK in regard to generative AI’s massive appetite for infrastructure and power generation: “BlackRock is at the center of the investment opportunity being shaped by the demand for generative AI. AI cannot truly happen without investments in infrastructure. These technologies require a new generation of upgrade data centers, which will need enormous amounts of energy to power them. With the AI-fueled need to build data centers, we see great potential to monetize the 4.3 gigawatts of power production capacity of generational assets currently owned by BlackRock's infrastructure funds.”

I’m definitely holding my current 2.0% allocation to BLK. As mentioned, I do want financial services exposure and I think BLK is a great way to get that diversification without directional interest rate exposure. As the earning season progresses, I’ll consider adding.

In this context, by “actively managing” I simply mean that my equities portfolio is a large set of individual stocks that I buy or sell individually. As opposed to, say, a set of ETFs or index funds. I believe in asset allocation, I’ve lost my religion for stock-specific alpha. In this respect, I can only really manage risk.

I’m serious. I should be doing my python homework right now.

What I mean is: I might asset allocate to growth, real estate (REITs), and other factors, then I could generally track his portfolio for my growth allocation. He not only works harder than me, he’s obviously a much better investor. Maybe it’s better to allocate this way as my own fund-of-funds, except I don’t need to charge myself an extra layer of fees!

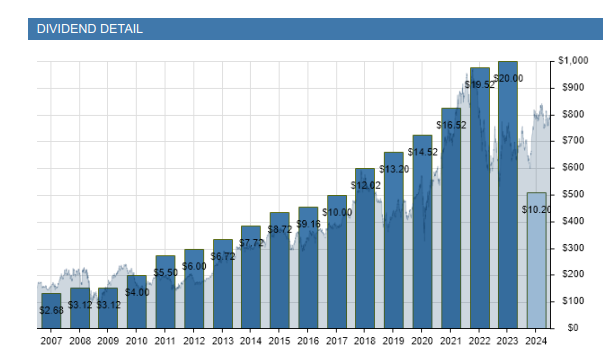

Dividend detail, see linked Stock Rover research report.

Via their explicit permission to share. Here’s more information about their Research Reports: https://www.stockrover.com/help/introduction/research-reports/ Frankly, I can’t recall if my (unlimited reports) are grandfathered into my longtime Premium Plus subscription. I don’t use these Reports too often: the Stock Rover platform has incredible customizability and daily integration with my Merrill Edge portfolio.

As Daniel Urbina accurately writes, “It's evident that BlackRock suffers from the law of large numbers when they are the largest asset manager and holds double-digit trillions of dollars in AUM. That's why it is smart to display some attention to non-core segments for growth such as alternative investments and software solutions to increment those growing percentages … For them to grow their AUM by 100%, they need another $10 trillion, and that can't simply occur organically without the help of economic growth and expansion in the money supply.”